Can We Talk About Interest Rates?

This guest commentary is part of a larger series where CCB periodically invites external colleagues to write on an issue they’re passionate and knowledgeable about.

By Bruce Mirken

If you follow economic news at all, you’ve no doubt heard that the Federal Reserve has been jacking up interest rates in an attempt to curb inflation. That raises a lot of issues, and over the summer CCB’s CEO Adam Briones wrote an op-ed for The Hill about how higher mortgage rates could slam the door shut on homeownership opportunities for communities of color and for working families more broadly. That hasn’t changed.

But here’s another aspect of the interest rate rise that’s gotten just scattered notice in the media: Not all rates are going up equally.

The Fed’s main tool for impacting interest rates is by setting what’s called the federal funds rate – what banks charge to lend each other excess cash overnight. It’s varied a lot over the past 75 years. After being close to zero for a couple of years as the Fed tried to keep the pandemic from crashing the economy, it’s jumped up this year, so it now sits in a range from 3.0% to 3.25%. That has, as intended, rippled through the economy, leading to higher rates for everything from home mortgages and auto loans to the interest paid on government bonds (more on that in a bit). The interest rate on a 30-year fixed-rate mortgage, for example, hit 6.7% in late September, rising 1.5 points in just six weeks.

You know what hasn’t risen nearly so much? The interest rate banks pay you on your savings account.

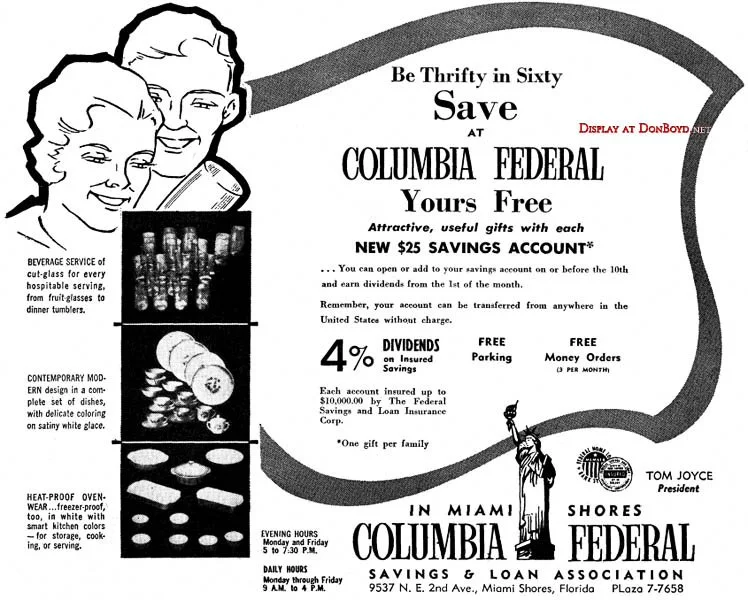

Savings Interest Rates Used to Be Much Higher

Being of – ahem – a certain age, I can remember back to the mid-1960s when the federal funds rate was in the same general range as it is now – a bit higher or lower at times, but generally close -- and banks and savings and loans were advertising interest rates on regular savings accounts of 4.5% or higher. These weren’t CD rates with long terms and early withdrawal penalties, just regular, garden-variety savings accounts.

In southern California where I grew up, I remember a bit of an interest rate war circa 1965-6 or so. One outfit bumped its savings rate to 4.8% and almost immediately Great Western Savings, where my parents had accounts, had big posters in their window advertising 4.85%. Take that, competitor!

(You might wonder what sort of weird child remembers interest rate ads from when they were nine. If I had a therapist, perhaps they could answer, but in any case, this stuff has stuck in my mind.)

I wasn’t able to find images of those Great Western posters, but just a bit of online searching located a number of early 1960s ads from other institutions touting similar rates, as you can see from the illustration. These weren’t outliers. Back then, savings account interest rates in the 4-5% range were routine.

Now, things are rather different. As of November 15, Bank of America – to pick one prominent example – was offering savings account interest rates ranging from 0.01% to 0.04% in the Bay Area. CD rates reached a whopping 0.05%. Wells Fargo’s rates were similar. Both did offer special, promotional CDs with returns in the range of 2-3% if you meet the minimum deposit requirement, but there’s a catch: This relatively high rate only applies for an initial term, generally from seven to 13 months, then the account rolls over into a regular CD with interest calculated in the hundredths of a percent.

This isn’t to pick on those two banks. They’re pretty typical of what’s out there. A few institutions – often online-only fintech firms -- do offer higher rates, but they’re pretty scarce and you have to hunt for them.

Something new is going on here: From 1960 to 1966, the federal funds rate ranged from about 1.2% to 5.75% and was mostly in the 3-4% range, pretty similar to late 2022. And yet savings account interest rates were orders of magnitude higher than they are now. What’s up with that?

The leading explanation seems to be that because many Americans saved their pandemic relief money, banks have more deposits on hand than they need to fund the loans they make. I don’t know whether that fully explains it, but if so, it suggests that working families aren’t going to see rising interest on their savings anytime soon. If any enterprising economics or consumer affairs reporters out there want to investigate further, California Community Builders would be happy to help any way we can.

If You Have Money, You Can Do Better

And this points to another problem: If you have significant savings, you can put your money into other sorts of investments that pay much better than bank accounts. But those investments really only work for people with substantial assets – enough money put away that they don’t need to keep all of it instantly accessible for sudden emergencies.

My own situation, if you’ll indulge me, offers a good illustration. I’m semi-retired, a status made possible by lucky circumstances that allowed me to accumulate a chunk of money that I then invested in federally tax-exempt government bond funds. These funds buy bonds issued by various government entities and pay dividends to shareholders based on the interest they collect on those bonds. There’s risk involved: Bond prices go up and down, as do the share prices of the funds. If you have to sell when prices are down, you take a hit, so this isn’t where you put cash you might need quickly for an unexpected emergency.

This year’s rapidly rising interest rates on government bonds have already boosted my monthly dividend payments by nearly 8%. It’s not enough to make me rich, but it’s enough each month to take myself out to a really nice dinner.

I can take advantage of this because I have a pool of money I don’t need to be able to access quickly – I have other funds tucked away in a low-paying bank account to handle an unexpected car repair, roof leak or whatever. The investments that pay well are not designed for people putting a small amount of money away each month in case of emergency – the retail worker, say, making $16 an hour and lucky to be able to set aside $50 at the end of each month. Those folks – and because of the huge racial wealth and income gaps, they’re more likely to be Black, brown or indigenous – are stuck with conventional bank accounts paying literally pennies.

Rethink Policy on Interest Rates

Once again, our financial system isn’t working for working families. So, what do we do? I don’t have anything like a complete answer, including a solution to the savings interest rate dilemma, but a starting point might be: Let’s stop making things worse. Rising interest rates show every sign of making things worse for most Americans.

As economist J.W. Mason wrote recently in the financial news outlet Barrons, “Over the past three months, housing costs accounted for a full two-thirds of the inflation in excess of the Federal Reserve’s 2% target.” And, he explained, “Conventional monetary policy is ill-suited to tackle rising housing prices” because high rates can reduce housing production, which depends on access to credit. “Economics 101 should tell you that if efforts to reduce demand are also reducing supply, prices won’t come down much. They might even rise.” In short, by raising rates, the Fed might be making the housing affordability crisis worse, not better.

Sen. Elizabeth Warren argues correctly that the way to benefit real Americans – not the super wealthy – is by “lowering housing costs by increasing [housing] supply,” along with other important steps like increasing affordable child care and tackling corporate price gouging. Most of that agenda isn’t in the Fed’s purview, but our political leaders can take action.

Let’s lean into solutions that will truly help working families without increasing the burdens on already vulnerable communities.

Bruce Mirken is a long-time writer and activist whose work has been published all over the U.S. and who previously led media relations for The Greenlining Institute and the Marijuana Policy Project. He now assists California Community Builders with strategic communications initiatives.

* * * *